Answering the question of how do VCs assess founders requires moving away from historical pattern matching and embracing the objective measurement of a founding team’s soft power.

How do VCs assess founders?

The venture capital world can be seen as a paradox. While it is an asset class built on future investment, its processes of finding the creators of the future – startup founders – still rely heavily on the past. The very essence of the business model used in venture capital is driven by power-law distribution. In other words, there are only a few successful companies in every VC fund, which brings a sense of constant risk associated with finding a few outliers. As a result, the evaluation process of what can be considered the most important element of startup success, the founder himself/herself, should become highly scientific.

Unfortunately, despite having powerful tools when it comes to assessing the market and developing financial projections, VCs’ efforts to evaluate human capital are still based on a set of heuristics. While such an “assessment gap” can be considered a problem in itself, it actually becomes the number one reason why, between 2019 and 2024, $1.2 trillion worth of venture capital has gone up in flames. When analyzing post-mortem cases involving thousands of startups that have failed during their first two years, it becomes evident that 60-70% of them do not fail because of technical problems and competitive challenges but rather due to preventable human error: dysfunctional management, co-founders’ conflicts, misalignment with market needs, etc.

The obvious follow-up questions then would be: how do VCs assess the founder’s potential, and what is the nature of the systemic problem in their process which allows such losses of capital to happen? These questions are the key focus of this essay as it examines the traditional VC evaluation toolkit from the perspective of behavior science and introduces a new concept of assessing the founder’s “soft power.”

While there are advanced approaches and methods available in relation to market sizing and financial modeling, there is an aspect called “human capital assessment,” which continues to operate on the basis of heuristics. The lack of sophistication in evaluating and assessing human capital is hardly a minor challenge—it can be regarded as the major factor behind the estimated amount of $1.2 trillion in venture capital lost between 2019 and 2024. Postmortem studies have found out that up to 60-70 percent of startup failures were caused by avoidable mistakes related to poor management, conflicts between co-founders, disconnect from the ground reality, and making poor decisions under stress.

The question that follows logically is: how do venture capitalists evaluate founders? How are their methods flawed in terms of assessing human capital? In order to address this issue, this paper will explore the toolkit used by venture capitalists, uncover some of its weaknesses based on behavioral science theory, and introduce a new approach to founder evaluation, relying on the objective measurement of soft power.

The Traditional VC Toolkit: An Art of Proxies and Pattern Matching

Venture capitalists, particularly seasoned partners at established firms, have honed a set of evaluation techniques over decades of experience. These methods are not without merit; they are designed to filter thousands of opportunities down to a handful of investable ventures with speed and conviction. However, they are fundamentally reliant on proxies for competence rather than direct measures of it.

Pattern Matching and Pedigree: The most common heuristic is pattern matching. VCs look for founders who fit a profile that resembles past successes. This often translates to a checklist of prestigious credentials: a computer science degree from Stanford, a stint as a product manager at a FAANG company, or a previous successful exit. The network itself becomes a filter, with “warm introductions” from trusted sources serving as a powerful initial signal.

Scientific Shortcoming: The method is riddled with problems related to survival bias and affinity bias. It aims at picking founders based on similarities to former successes and consequently fails to pick up new founder types, thus being non-diverse. It confuses correlation (winners frequently have these pedigrees) with causality and disregards the huge population of such people that didn’t succeed despite having these attributes. Having a pedigree is an indicator of access and education but does not indicate resiliency, adaptability, or good decision-making skills in tough times.

Pitch Meeting and Storytelling Skill: The pitch meeting is at the heart of the founder assessment. Here, venture capitalists judge whether or not a founder can tell an engaging story, express big visions, and answer hard questions. Charisma and skillful storytelling are perceived as traits of leadership and an ability to recruit people around you and sell to customers.

Scientific Limitation: Here, there is a problem with confusing competence with performance. It works great for testing salespeople, but not very well for evaluating competence in operations or ethics. The failure of a startup like Theranos headed by a highly charismatic Elizabeth Holmes serves as a good example. An approach that emphasizes a founder’s storytelling skills over his real abilities is tailor-made to be fooled by narcissistic leaders and ignore talented but introverted entrepreneurs.

Assessing Market and Idea: VCs spend a lot of their time estimating the size of total addressable market, the uniqueness of the concept and the unique value of a product being offered.

Scientific Limitation: This analysis is often conducted based on the founder’s own projections and assumptions. Without an objective measure of the founder’s cognitive power and signal-detection ability, the VC has no way of knowing if the TAM is realistic or a hallucination born of confirmation bias. The idea is inseparable from the founder’s ability to validate and execute it. A brilliant market opportunity in the hands of a founder who lacks ecosystem awareness is worthless.

The fundamental flaw uniting these methods is their susceptibility to cognitive biases—on the part of both the founder and the investor. The halo effect can cause a VC to view a founder with a Stanford degree as competent in all areas, while confirmation bias can lead them to seek data that validates their initial “gut feeling” about a deal. The question, how do VCs assess founders?, is thus answered: often, by using their own flawed cognitive systems to evaluate another’s.

Startup Founder Soft-Power Assessment: The Unmeasured Universe

The traditional toolkit leaves a vast and critical domain of founder capability almost entirely unmeasured: their “soft power.” As defined by the Supsindex framework, soft power is the non-technical, human-centric weave of knowledge, behavior, and contextual awareness that ultimately determines execution quality. This is where the majority of startup failures originate. A true Startup Founder Soft-Power Assessment must move beyond proxies and measure these capabilities directly.

The current methods fail to answer the most important questions:

- Does the founder possess the actual entrepreneurial literacy to understand unit economics, or are they just repeating jargon from a blog post?

- What is the behavior of the founder when they realize their most significant client is leaving them and they only have three weeks left to save themselves?

- Do they panick, analyze, or deny?

- Do they have the behavioral synergy needed to navigate through the pivot, or will it turn into their Achilles heel due to the complementary behavior of each other?

- Does the founder really know about the regulations within Germany regarding healthtech, or are they using the same playbook used by American SaaS companies?

These are not questions that can be answered by looking at a résumé or a pitch deck. Answering them requires a new class of assessment tools.

Founder behavioral data for VC: Moving from Self-Reporting to Simulation

In order to mitigate the risk arising out of the human factor, the venture capitalists need objective data about how the entrepreneurs behave in order to make VC-level decisions. The kind of information that needs to be acquired cannot be obtained through the subjective measures that can be used to measure an entrepreneur’s personality via questionnaires such as the MBTI or even the Big Five Personality model. What science requires is the evaluation based on behavior rather than personality. The Supsindex approach represents an innovative shift here.

The General Entrepreneurial Behavior (GEB) test is not designed to evaluate personality; instead, it is an algorithm for evaluating behavioral decision-making skills. It uses a forced choice paradigm based on the Thurstonian Item Response Theory that requires entrepreneurs to make decisions about what action among a few realistic options would be the best and the worst in a given real-life situation.

What this does:

- It reduces social desirability bias: By forcing a choice, it does not allow the user to just give themselves the best ratings across the board.

- It Detects Cognitive Biases: The “least effective” options are often engineered to be socially desirable but strategically flawed traps. For example, a micromanagement bias might be disguised as “supportive checking-in.” A founder’s ability to consistently reject these traps in favor of more effective, if less virtuous-sounding, actions provides powerful founder behavioral data for VC analysis.

This “Dual Engine” approach not only measures the strengths of the founder, such as Achievement Drive and Resilience but also their risk factors, such as vulnerability to the Overconfidence Bias effect. It creates a rich behavioral profile that is more predictive than the simple categorization of personality type.

Commerce, moreover, goes well beyond testing factual knowledge alone. With Item Response Theory and Signal Detection Theory applied, using questions weighted for difficulty and including “distractor” questions as well, it tests a founder’s ability to filter out the important signals about their business amidst all the noise. This assesses an individual’s cognitive processing abilities under conditions of overload – a vital skill set that most assessments do not address. This is how a genuine Startup Founder Soft-Power Assessment looks like.

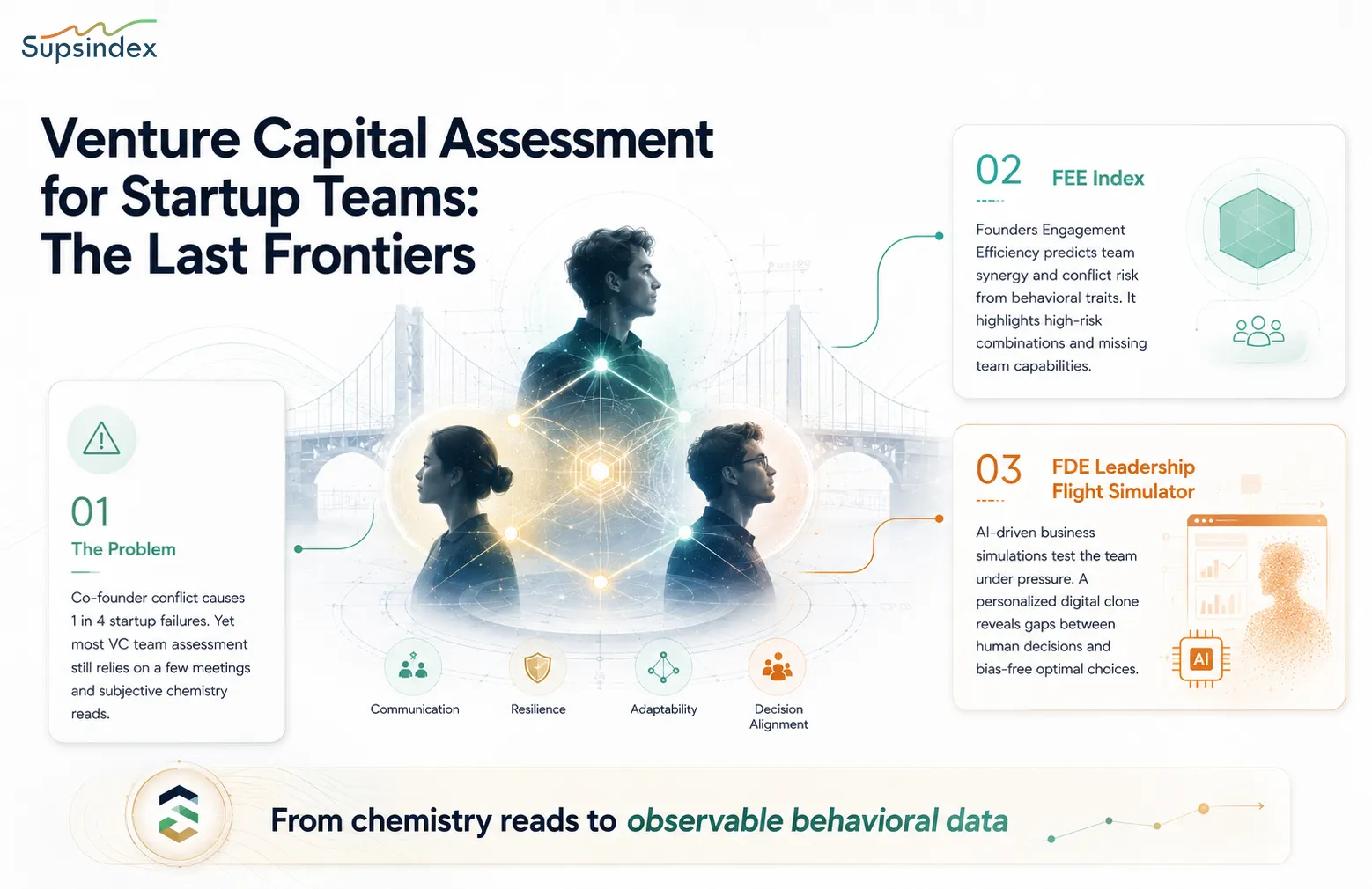

Venture Capital Assessment for Startup Teams: The Last Frontiers

Certainly, one of the largest oversight areas in venture capital relates to the assessment of the founding team as a whole. Conflict between co-founders contributes to the demise of one in four startups, yet the standard Venture Capital Assessment for Startup Teams consists of barely a handful of meetings to assess chemistry alone. This is akin to predicting the structural integrity of a bridge by observing the color of its paint.

Science needs to recognize that teamwork represents a complicated system whose performance emerges from the interaction of its components. Two revolutionary instruments have been developed within Supsindex for this purpose, namely:

- Founders Engagement Efficiency (FEE) Index: This index goes beyond mere individual analysis and enables prediction of how well team members will engage. Through assessment of the behavioral traits of each member of the team based on GEB, the index is able to identify the likelihood of both synergistic teamwork and conflicts between the members. The index may, for instance, point out high-risk combinations, such as highly dominant risk-averse individuals, or lack of critical abilities such as a group of visionaries who lack Organized and Delegation Abilities.

- Founder Decision Excellence “Leadership Flight Simulator”: This is where the pressure is highest. The FDE uses artificial intelligence and simulations to put all of the founders through a series of business scenarios. These are simulated problems that increase in complexity over the course of several hours. The most revolutionary aspect of the FDE is the Personalized Digital Clone. Based on the team’s prior assessment data, Supsindex creates an AI twin that represents the team’s optimal, bias-free decision-making potential. The FDE platform tracks the divergence between the stressed human team’s decisions and the rational choices of their digital clone.

This provides an unprecedented, objective measure of a team’s decision quality under pressure, their communication breakdowns, and their collective resilience. It answers the question that keeps every VC up at night: “How will this team actually behave when things go wrong?” This simulation-based approach is the future of Venture Capital Assessment for Startup Teams. It replaces subjective “chemistry reads” with hard, observable behavioral data.

Conclusion: What Are the Keys for VCs to Assess Founders?

Returning to our primary question, it is evident that venture capitalists assess founders using an incomplete and obsolete toolkit that does not account for human characteristics and leaves them unaware of the primary causes behind the majority of startups’ failures. This approach cannot serve as an efficient and reliable solution anymore in light of the increasing investment volume.

In order to improve founders’ evaluation process in the coming years, VCs should abandon subjective heuristics in favor of scientific methods that involve objective data collection and analysis. Namely, it means a paradigm shift from resume-based assessment to the evaluation of cognitive systems and behavior patterns; the consideration of a person’s skills separately should be replaced by modeling startup teams’ interactions.

The implementation of the proposed Startup Founder Soft-Power Assessment framework will provide venture capitalists with an innovative toolkit that allows for creating an accurate picture of a founding team’s potential through a combination of FPA, GEB, EEA, FEE, and FDE tests. In such way, investors will be able to avoid pattern matching while making more confident decisions. The involvement of objective criteria and data analysis will transform VCs from amateur gamblers into professional investors in the area of human capital management.

The global innovation economy has come to a crossroads. The cost of failure associated with the lack of appropriate tools to identify it is too high, which is why venture capitalists are encouraged to update their practices in a timely manner. To explore the scientific methodologies and validated indices that are making this new paradigm of founder assessment a reality, the frameworks being developed at Supsindex offer a glimpse into the future of data-driven investment.